Key Data Points for Informed Decision-Making

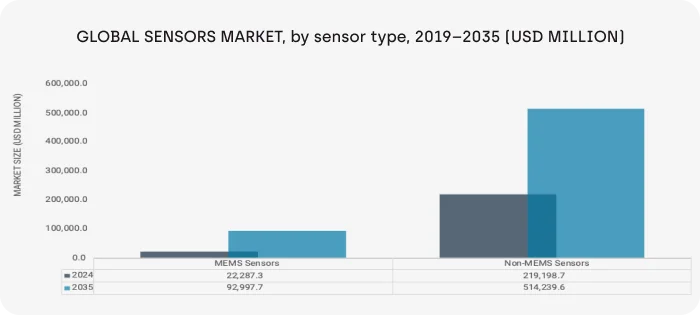

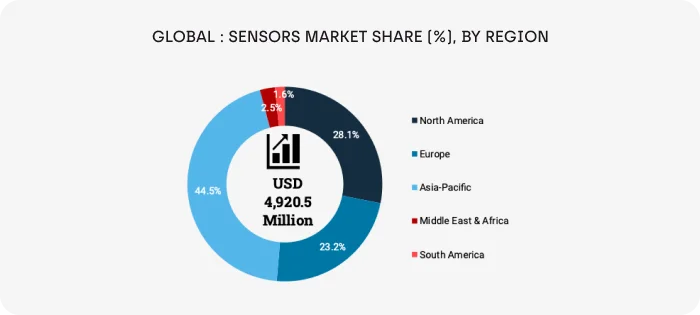

Key data points for informed decision-making in the global sensors market include market size, growth rate, and segmentation by type (e.g., temperature, pressure, motion, optical, image, biosensors), technology (MEMS, CMOS, IoT-enabled, wireless), and end-use industries such as automotive, consumer electronics, healthcare, industrial automation, aerospace, and defense. Regional trends particularly the dominance of Asia-Pacific in manufacturing and North America in innovation are essential for strategy alignment. Competitive landscape insights, including leading players, emerging startups, M&A activity, and R&D investments, provide a clear view of market positioning. Supply chain dynamics, raw material dependencies, and semiconductor shortages also shape growth potential. Additionally, technological advancements such as AI integration, miniaturization, and edge sensing are critical drivers, while regulatory frameworks, environmental sustainability, and data security compliance influence adoption. These data points collectively help businesses identify growth opportunities, mitigate risks, and refine go-to-market strategies in the evolving sensor ecosystem.

The regulatory landscape for the global sensors market is driven by stringent standards to ensure safety, reliability, and environmental compliance. Key regulations include ISO certifications, RoHS and REACH directives in the EU, and FCC/CE approvals for electronic communication-enabled sensors. Healthcare sensors must meet FDA and EU MDR requirements, while automotive sensors comply with ISO 26262 safety standards. Additionally, cybersecurity frameworks like GDPR and NIST shape IoT-enabled sensors, making regulatory adherence critical for market access, innovation, and competitive positioning.

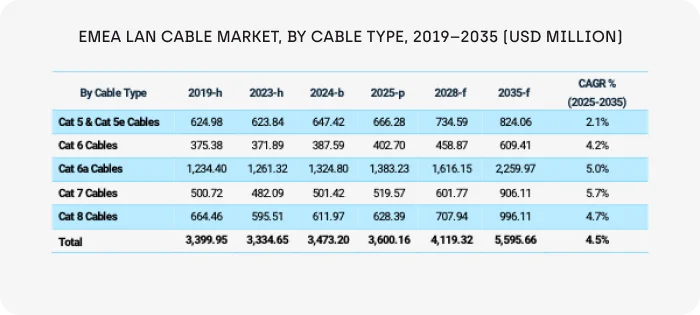

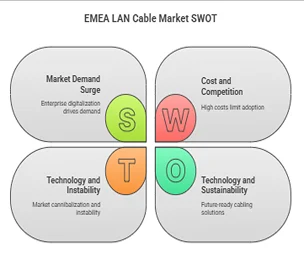

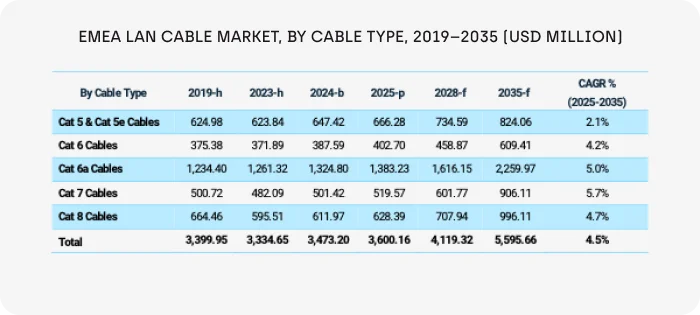

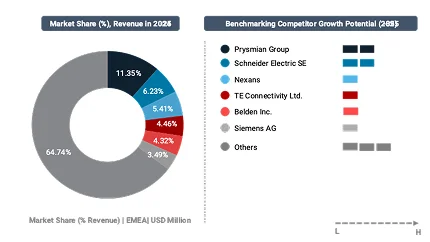

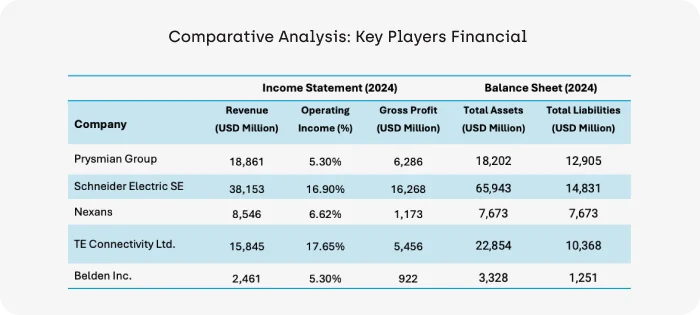

Driving Connectivity: Competitive Dynamics in the EMEA LAN Cable Market

The EMEA LAN cable market features a highly competitive landscape, marked by a mix of global industry leaders and regional specialists. Key players such as Prysmian Group, Nexans SA, Belden Inc., TE Connectivity, and others dominate market share through extensive product portfolios, strategic investments, and ongoing innovation in both copper and fiber cable technologies. The market continues to fragment as fast-scaling startups and smaller regional manufacturers compete by offering customized solutions and agile services, driving diversification in product offerings and pricing. This dynamic environment accelerates advancements in connectivity, with established companies focusing on expansion and tech upgrades to sustain their competitive edge in EMEA.

Thank you for Reading